Comprehensive Analysis of Stablecoin Transfers, Compliance, and Ecosystem Dynamics

For more insights into stablecoin market dynamics, you may also be interested in our previous report analyzing illicit activity patterns in USDT and USDC transactions.

1.Abstract

2.Scope of Research

In this report the following three top stable coins are analyzed: USDT, USDC and BUSD. In particular:

- History, Transacting Volumes and Users.

- Timeline of Statistics Along With Some Key Dates.

- Usage Patterns and Flows Between Major Types of Agents.

- Possibilities of Travel Rule Enforcement for Payments in Stable Coins.

3.Definitions

3.1. Stable Coin

A stablecoin is a type of cryptocurrency designed to have a stable value. This stable value is typically pegged to a reserve or benchmark, such as a specific amount of a commodity (like gold) or more commonly, a fiat currency (like the US dollar). The primary purpose of stablecoins is to provide the benefits of digital currency – such as fast transactions, privacy, and security – without the high price volatility typically associated with cryptocurrencies. There are several mechanisms used to achieve this stability:

- Fiat-Collateralized Stablecoins: These are backed by a reserve of fiat currency, typically held in a bank or a trusted third-party. For every stablecoin issued, there is a corresponding unit of fiat currency held in reserve. Examples include USDC and Tether (USDT) and BUSD.

- Crypto-Collateralized Stablecoins: These are over-collateralized by other cryptocurrencies, such as Ether. If the value of the collateral drops, mechanisms are triggered to ensure the stablecoin's value remains stable. A popular example is DAI, which operates on the Ethereum platform.

- Algorithmic Stablecoins: These are not backed by collateral but instead use algorithms and smart contracts to automatically adjust the supply of the stablecoin, increasing or decreasing it in response to changes in demand to maintain its peg. Examples include Ampleforth (AMPL) and Terra (LUNA).

3.2. Stable Coin Collateral

Collateral is a reserve of fiat currency, typically held in a bank or a trusted third-party. Could also be money surrogates, Bonds, Treasuries, sometimes even shares of companies following stock market indexes (like Vanguard (VOO) for SNP500).

3.3. Stable Coin Depeg

In this research we’ll be analyzing the fiat-collaterized stable coins. Depeg is an event when stablecoin market value deviates from the fiat currency they're pegged to, often due to factors such as:

- Doubts About the Actual Reserve Backing

- Mismanagement by the Issuing Entity

- Regulatory Pressures

- Sudden, Large Redemption Requests.

In such scenarios, if traders believe that the stablecoin doesn't truly have a 1:1 fiat reserve as claimed, or if they suspect they might face challenges redeeming the stablecoin at its full value, they might sell off their holdings, leading the stablecoin's value to drop below its intended peg.

3.4.Stable Coin Holder

Holder is a person or a smart contract which “holds” some amount of Stablecoins on its address. Holder can transact in Stablecoins with other Holders.

3.5.Centralized Exchange (CEX)

A centralized exchange is a platform where users can buy, sell, or trade cryptocurrencies and, in some cases, fiat currencies. Key characteristics of centralized exchanges include:

- Custodial: Centralized exchanges hold users' funds, either in fiat or cryptocurrency, in their custody. When you deposit funds into a centralized exchange, you're essentially entrusting them with the safekeeping of your assets.

- User Accounts: To trade on a centralized exchange, users typically have to create an account and undergo a Know Your Customer (KYC) verification process, which involves providing personal details to comply with regulations.

- Order Books: These platforms use order books to match buyers and sellers. Users place market or limit orders, which are then matched by the exchange's trading engine.

- Interface: Centralized exchanges often provide user-friendly interfaces, charting tools, and other trading resources, making it easier for both novice and experienced traders.

- Liquidity: Due to their popularity and user base, centralized exchanges often have high liquidity, making it easier to execute large trades without significantly affecting the market price.

- Fees: Centralized exchanges typically charge fees for trades, deposits, or withdrawals. The fee structure can vary based on the platform and the user's trading volume

- Security: While CEXs implement robust security measures to protect user funds and data, they have been targets of hacks in the past. As a centralized point of failure, they can be more vulnerable than decentralized systems.

Examples of popular centralized exchanges include Binance, Coinbase, Kraken, and Bitfinex.

3.5.1. CEX Hot Wallet

Hot wallet is an address where CEX entity keeps its Stable Coins (liquidity) available for immediate withdrawal by users. From the business perspective, CEX uses Hot Wallet to service immediate users withdrawal and collects deposits onto this address. This wallet is usually integrated with CEX information systems for business operation purposes and thus can be compromised in event when the information system is compromised, resulting in funds draining by hackers.

3.5.2. CEX User Deposit Address

Because of the fact that a payment (or transfer) in StableCoin doesn’t have “payment description” field, there is no way for CEX to distinguish between different users depositing their Stablecoins. To mitigate this issue, CEX creates a so-called “User Deposit Address”, which is essentially a personalized unique address dedicated to accept stablecoins from exact one user. This essentially results in a fact, that CEX uses not a single wallet users transact with, but a large number of wallets for different purposes.

3.6.Decentralized Exchange

A decentralized exchange (DEX) is a cryptocurrency trading platform that operates without a central authority or intermediary. Instead of relying on a centralized entity to facilitate trades, DEXs use blockchain technology, primarily in the form of Smart Contracts, to automatically match buy and sell orders. Key characteristics of decentralized exchanges include:

- Non-Custodial: DEXs do not hold or have custody of users' funds. Instead, trades are made directly from one user's wallet to another.

- No KYC: Most DEXs don't require users to undergo a Know Your Customer (KYC) verification process, ensuring greater privacy and anonymity.

- Smart Contracts: DEXs rely on smart contracts to facilitate and verify trades. This automation ensures that the terms of the trade are executed precisely as agreed upon.

- Liquidity: Early DEXs faced challenges related to low liquidity, making it harder to execute large trades. However, the introduction of liquidity protocols and pools, like those used in Uniswap or SushiSwap, has addressed some of these concerns.

- Interoperability: Some DEXs are designed to be interoperable, allowing for trades across different blockchains or networks.

- Fees: DEXes also may charge fees from each trade, but users also have to pay “gas fees” separately for the execution of smart contracts on the blockchain network, especially on platforms like Ethereum. Which makes usage of DEXes more expensive compared to CEXes.

- User Experience: Initially, DEXs were seen as less user-friendly compared to centralized exchanges. However, with the evolution of the DeFi (Decentralized Finance) ecosystem, many DEX platforms have become more intuitive and user-centric.

Examples of popular decentralized exchanges include Uniswap, SushiSwap, PancakeSwap, and Balancer.

4.Historical Overview of Major Fiat-Collateralized Stablecoins

4.1.Historical Overview

4.1.1.USDT (Tether USD)

– 2014-2015: Birth and Early Days

Tether was originally conceived in a whitepaper titled "The Mastercoin white paper" by J.R. Willett in January 2012. The implementation of Tether on the Mastercoin protocol became the predecessor to the Omni Layer, a platform for creating and trading custom digital assets on the Bitcoin blockchain. Tether was launched in July 2014 as "Realcoin" by Brock Pierce, Reeve Collins, and Craig Sellars. A short while later, it rebranded as "Tether" and introduced the USDT ticker. The primary proposition was simple – every USDT token was purported to be backed by one US dollar held in reserve. This 1:1 peg was designed to combine the stability of the U.S. dollar with the technological advantages of cryptocurrency.

–2016-2017: Adoption and Controversy

Tether began to be integrated into several prominent cryptocurrency exchanges, like Bitfinex, which led to increased adoption and use. Concerns began to arise regarding whether Tether actually held enough U.S. dollars to back all USDT in circulation. Additionally, the close relationship between Bitfinex and Tether (they share key executives) was spotlighted, particularly after issues related to banking access and wire transfers.

–2018: Intense Scrutiny and Legal Battles

Tether's banking relationships came under the spotlight. Initially, Tether had difficulties with banking partnerships, moving from one bank to another. The community grew more skeptical about Tether's dollar reserves. Although Tether claimed every USDT was backed by a dollar, they discontinued relationships with auditors before a full audit could be presented.

– 2019-2020: Legal Investigations and Partial Backing Admission

NYAG Investigation: The New York Attorney General (NYAG) began investigating Bitfinex and Tether, suggesting that a cover-up had taken place to hide a loss of funds.

Backing Admission: Tether modified its claims in 2019, stating that USDT was not only backed by cash but also by "cash equivalents" and "other assets and receivables from loans."

–2021 and Beyond:

Legal Settlement: In 2021, Tether and Bitfinex settled with the NYAG, agreeing to pay $18.5 million in damages and being transparent about reserves. They did not admit to any wrongdoing.

4.1.2. Current State

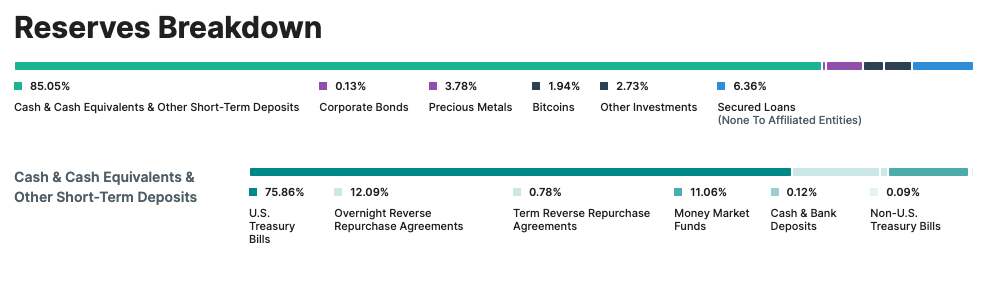

Reserves: According to latest report (dated June 30, 2023), Tether reserves are distributed the following way:

- Treasury Bills: 75,86%

- Overnight Reserve: 12,09%;

- Market Funds: 11,06%;

- Secured Loans: 6,36%;

- Bitcoins and Other Investments: 4,76%

- Corporate Bonds, Funds & Precious Metals: 3,91%.

Total Emission: 86,6B USDT

Supported Blockchains:

- Ethereum (emission 39B USDT)

- Tron (emission 43,8B USDT)

- Binance chain (emission 3,37B USDT)

- Other Blockchain (with relatively low emission)

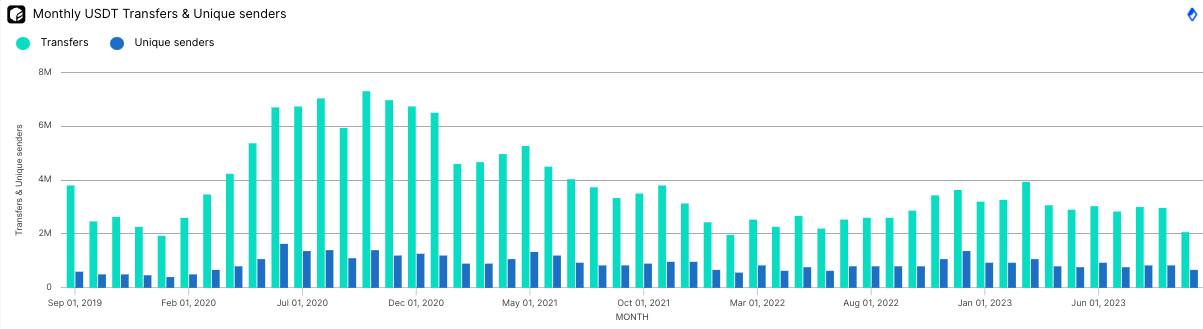

Transaction and Volumes:

- A significant spike in transferred volume is seen around Dec 2020-Jan 2021, at the beginning of the Bitcoin bull run. This could indicate more capital was flowing into the market, with investors possibly hedging with USDT.

- Post-Nov 2022, transferred volume sees a decline and remains subdued. This may suggest reduced market activity, even with a slowly rising BTC price, indicating uncertainty about the market's direction.

- In summary, the rise of DeFi era and consequently the Bitcoin bull run saw increased USDT transfers and volume, indicating heightened market activity and perhaps hedging, the bear market has led to consistent yet subdued USDT activity, reflecting market uncertainty and caution among traders.

- Transfers and unique senders surged around Feb 2020. This aligns with the onset of the DeFi era, suggesting increased adoption and activity in DeFi platforms.

- A noticeable decline in both metrics occurs after May 2021, during the middle of the bitcoin bull run. This could be because users held on to their assets anticipating higher returns.

- Post-Nov 2022, during the bear market's deep dive, both transfers and unique senders remain relatively stable, suggesting that even with declining BTC prices, USDT activity remained consistent, possibly as a safe haven for capital or because of the place of USDT in business activities that doesn’t depend on BTC price an not related to trading and speculation.

4.1.3. Summary

The significant increase of USDT usage in Ethereum Blockchain is matching the rise of the DeFi era, when USDT became one of the most used base asset to trade crypto assets with.

The fact that USDT activities remain consistent during Bitcoin low volatility time and bear market suggests that USDT has more usage rather than being just a base asset for trading on DEXes.

5.Stablecoin Flows Between Major Agent Types

5.1. Scope Definition

For this particular research, we’ll analyze the flows between CEXes, DEXes and Holder wallets. We’ll try to separate transfer operations based on transaction types which are dictated by the Ethereum architecture and technical decisions that founders use to build DEXes with. This will allow to separate at least 2 types of transactions thus separating traffic and money flows. For purposes of this research, we’ll be separately analyzing USDT in Tron and Ethereum blockchains due to the fact that they have comparable emission, but different usage patterns. Despite the same name, USDT in Ethereum and Tron are not directly interoperable and require bridging to convert one to another, which is nothing different from exchanging one token to another on exchange.

5.2. Technical Details

5.2.1 ERC20 Token Contract

Each stablecoin covered in this research is implemented in a form of a Smart Contract following the ERC20 standard and deployed in a particular EVM compatible blockchain. This standard defines the functions that user (Holder) may use to initiate transfers as well as a list of Events (logs) that are recorded when such a transfer has happened. In particular, it defines 2 functions that transfer may be initiated with:

function transfer(address _to, uint256 _value) public returns (bool success)

function transferFrom(address _from, address _to, uint256 _value) public returns (bool success)

In the context of this research, it’s important to mention that function “transfer” is used when user A is initiating a transaction from his account to user B, i.e. sending his/her tokens directly to User B. Such a transfer is usually called “Direct transfer”. Unlike the first function, the second one (“transferFrom”) is used when a User A wants to transfer tokens of User B to another account (usually his own), i.e. User A is charging some amount of tokens from User B’s account. This function is typically used when a Smart Contract wants to charge User for tokens, which is exactly what happens when User is transacting with DEX. These 2 different types of transfer initiation allows for separation of all the traffic of stablecoins into Direct Transfers and Charges. First type is used when people interact with each other or with CEXes, the second one is used when people interact with a decentralized platform (DEXes, Bridges, other DeFi platforms).

5.2.2. Token Standards in Other Blockchains

Token standards in different blockchain may (and usually) differ. But for purposes of this research, we’ll be referring to the TRC20 standard in Tron blockchain and BEP20 standard in Binance chain, which are literally a copy of ERC20 standard in Ethereum.

5.2.3. Address Labels

We’ll be referring to a set of address labels publicly available on research platforms like https://flipsidecrypto.xyz/ and blockchain explorers (https://etherscan.io, https://bscscan.com, https://tronscan.io). These labels include CEX Hot Wallets, DEX pools, routers and other well known public addresses.

5.3. USDT CEX and DEX flows in Ethereum

For purposes of this research we’ve analyzed USDT token usage in 2 dimensions:

- By Destination Address (which allows to understand in and out flows to CEXes and DEXes)

- By Transfer Initiation Function Type (which allows to understand exact type of operation performed)

- The Dataset Used Contains Transactions From Oct 2022 to Oct 2023. (1 year)

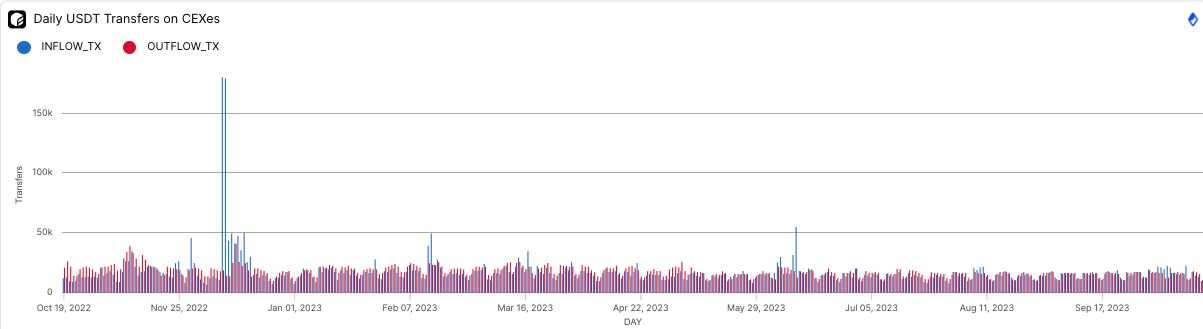

5.3.1.USDT CEX In/Out flows in Ethereum

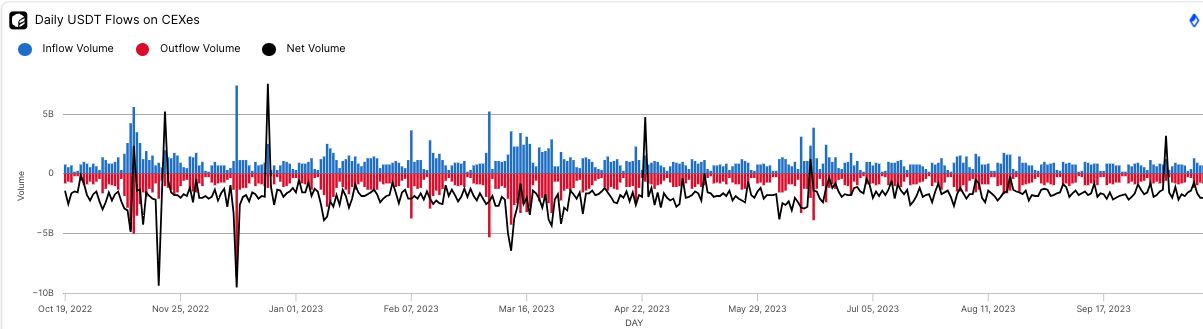

Daily USDT Flows on CEXes (Volume):

- Inflow Volume (Blue Bars): Represents the amount of USDT transferred from users to CEXes.

- Outflow Volume (Red Bars): Represents the amount of USDT transferred from CEXes to users.

- Net Volume (Black Line): Indicates the difference between inflow and outflow volumes. Positive values show more inflow than outflow, and negative values show more outflow than inflow.

Daily USDT Transfers on CEXes (Number of Transactions):

- Inflow Transactions (INFLOW_TX - Blue bars): Represents the number of transactions made from users to CEXes.

- Outflow Transactions (OUTFLOW_TX - Red bars): Represents the number of transactions made from CEXes to users.

Key Observations (Chronologically)

- End of Nov 2022:

- A significant spike in inflow volume.

- Correspondingly, there's a major rise in the number of inflow transactions.

- This activity might relate to anticipation of market movements following Bitcoin's "double" top bull run in Nov 2021.

- Mid-March 2023:

- Noticeable spike in both inflow and outflow volumes.

- Elevated activity in the number of inflow transactions.

- This correlates with the USDC 12% depeg event, which triggered panic sales in the market.

- Early June 2023:

- Another spike in inflow volume.

- Increased activity in the number of inflow transactions.

- This period matches the USDT 3% depeg event.

- General Observations:

- Most of the time, the net volume remains relatively stable, indicating a balanced inflow and outflow.

- Outflow transaction counts are consistent throughout the period with only minor fluctuations.

- These observations show the response of USDT transfers to and from CEXes during specific events in the cryptocurrency market.

5.3.2. USDT DEX In/Out flows in Ethereum

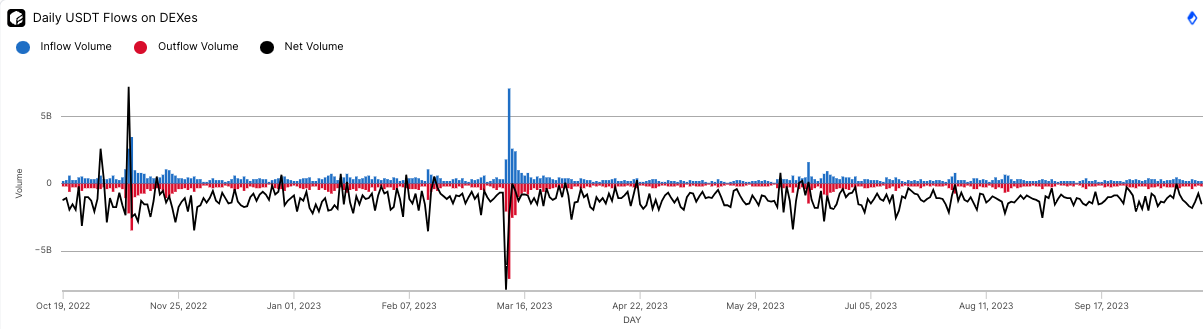

Daily USDT Flows on DEXes:

- Inflow Volume (Blue): The volume of USDT transferred from users to DEXes.

- Outflow Volume (Red): The volume of USDT transferred from DEXes back to users.

- Net Volume (Black): The net change in volume on DEXes. It's the difference between inflow and outflow.

Daily USDT Transfers on DEXes:

- Inflow Transactions (Blue): The number of transaction events where USDT is moved to DEXes.

- Outflow Transactions (Red): The number of transaction events where USDT is moved from DEXes to users.

Key Observations:

It’s important to note that Net Volume (Black) is negative most of the time. This indicates that users are tending to exit (selling assets) into USDT and fixing profits in this stable coin. Likewise, the down spike on Mar 13th means that users were rushing out of USDC into stable USDT in a panic sell.

- End of November 2022:

- Significant spike in USDT inflow volume to DEXes.

- Corresponding surge in inflow transaction counts.

- Positive Net Volume (Black) peak at this time corresponds to prevailing “Buying” assets operations rather than selling.This corresponds to lowest Bitcoin price during the latest bear market.

- Mid-March 2023:

- Exceptional spike in USDT inflow volume.

- Subsequent sharp decline in outflow volume.

- Unprecedented peak in inflow transaction counts.

- This activity is closely aligned with the March 10-11, 2023 USDC 12% depeg event, suggesting a relation or reaction to the event.

- Early June 2023:

- Noteworthy inflow volume spike.

- Elevated inflow transaction counts.

- This period coincides with the June 15, 2023 USDT 3% depeg event, hinting at a potential correlation.

- Outside these major events, inflow and outflow are generally balanced in terms of both volume and transaction counts.

The timing and magnitude of these spikes, especially around the USDC and USDT depeg events, suggest that users might have been reacting to market conditions by actively trading on DEXes which are capable of closing orders immediately comparing to order book based CEXes which are also likely to have their trading API “overloaded” during peak volatility time.

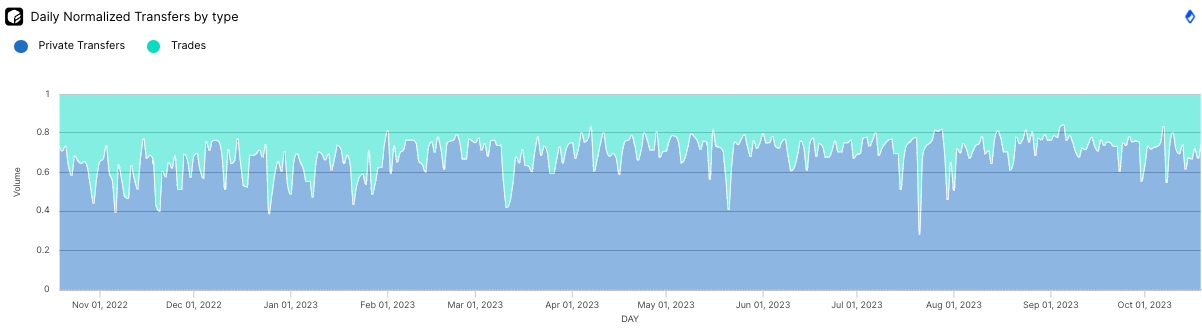

5.3.3.USDT Transfer types analysis in Ethereum

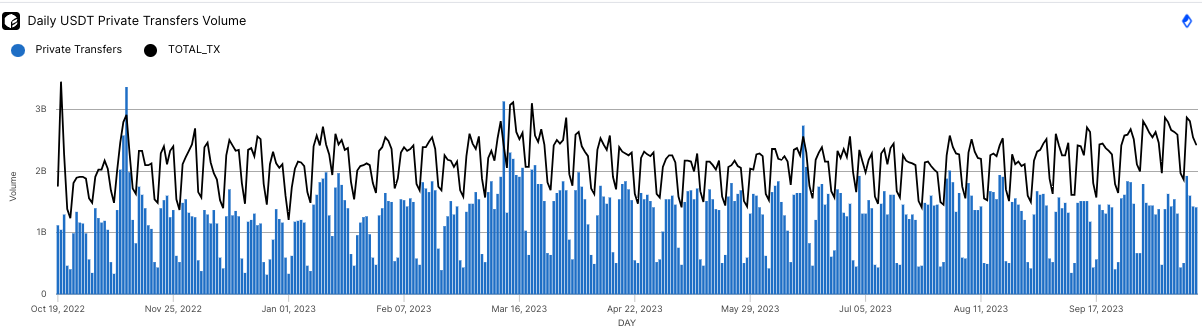

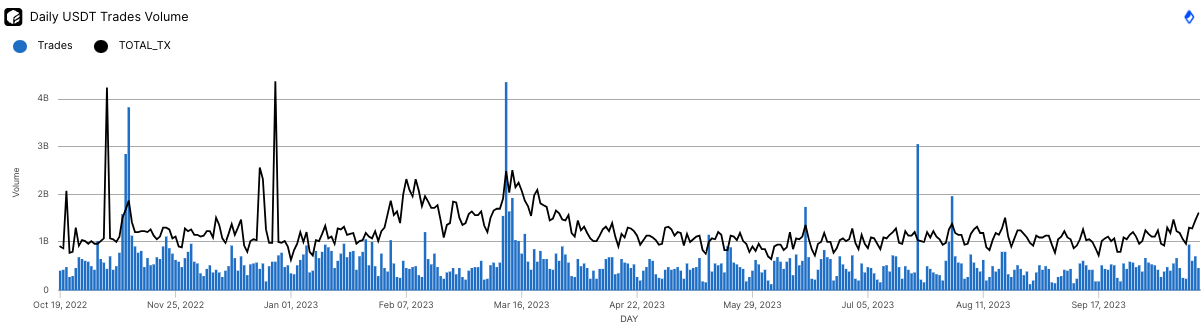

The top 2 charts in this chapter contain similar data but for different types of USDT transactions. First one is Trades volume (trading transactions on DEXes) and second one is Private Transfers (Direct transfers from User A to User B, including Deposit transactions to CEXes that are usually made by Direct Transfers).

Key Observations

- End of November 2022:

- Both charts display significant spikes around this time.

- Trades: Large surge in trade volume and transaction count.

- Direct Transfers: Substantial increase in private transfer volume, with a moderate increase in transaction count.

- Mid-March 2023:

- Trades: Exceptional spike in trade volume and transaction count.

- Private Transfers: A noticeable spike in volume and a mild surge in transaction count.

- Both activities around this period are consistent with the March 10-11, 2023 USDC 12% depeg event.

- Early June 2023:

- Trades: Significant spike in trade volume, elevated transaction count.

- Private Transfers: Moderate increase in volume, mild rise in transaction count.

- The spikes here align with the June 15, 2023 USDT 3% depeg event.

- General Observations:

- DEX Trades have more pronounced spikes in both volume and transaction count at key events than Direct Transfers.

- Direct Transfers exhibit a steadier volume with less drastic fluctuations than Trades.

- Trade volumes seem to be reactive, possibly reflecting market sentiment and reactions to external events. On the other hand, Private Transfers seem to represent more consistent and perhaps planned transfers between users.

- Other Notable Points:

- Around July 5, 2023, there's a clear spike in Trades but not as pronounced in Private Transfers.

- The two types of transactions offer insight into different aspects of user behavior. DEX Trades, being more volatile, may indicate market sentiment and reactions to news or events. In contrast, Direct Transfers seem more consistent and less reactionary, possibly showing planned transactions, remittances, or personal CEX deposits for future investments.

- The Private Transfer chart displays a clear weekly cyclical pattern, characterized by:

- Higher Volumes on Weekdays:

- There's a noticeable increase in the volume of private transfers during weekdays.

- This could be indicative of business-related transfers or professional transactions, which typically occur on working days.

- Decrease in Volume on Weekends:

- Volumes drop significantly during weekends.

- This trend suggests that fewer private transfers are made for business or professional purposes during weekends.

- Consistency of the Pattern:

- This cyclical pattern is consistent throughout the duration of the chart.

- Such a recurring pattern indicates that the behavior is not an anomaly but rather a reflection of regular user habits or practices.

- Higher Volumes on Weekdays:

The observed weekly pattern aligns with traditional financial practices where business activities, remittances, or professional transactions predominantly happen on weekdays, while weekends see a lull in such activities. It could also be indicative of the primary user base of USDT for private transfers, where a significant portion might be using it for business or professional reasons.

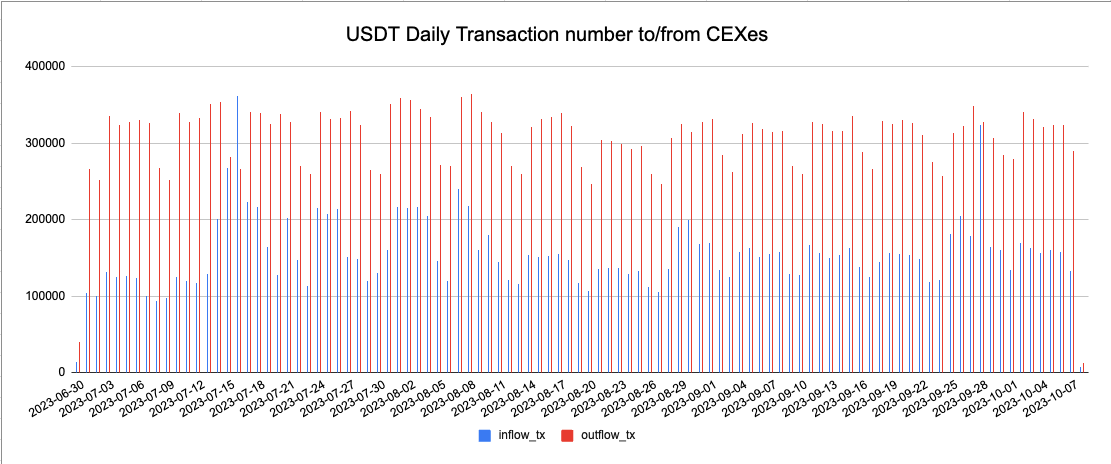

5.4. USDT CEX Flows in Tron

Unlike in Ethereum, USDT in Tron is mostly used for Direct Transfers (95%+ of transactions) leaving just 5% for DEXes. DEXes in Tron are not widely used and the majority of the users exchange USDT for TRX to pay for transaction commissions. Thus, for purposes of this research we’ve analyzed:

- In and Out Flows Onto Major CEXes

- The Dataset Used Contains Transactions From July 2023 to Oct 2023. (3 Months)

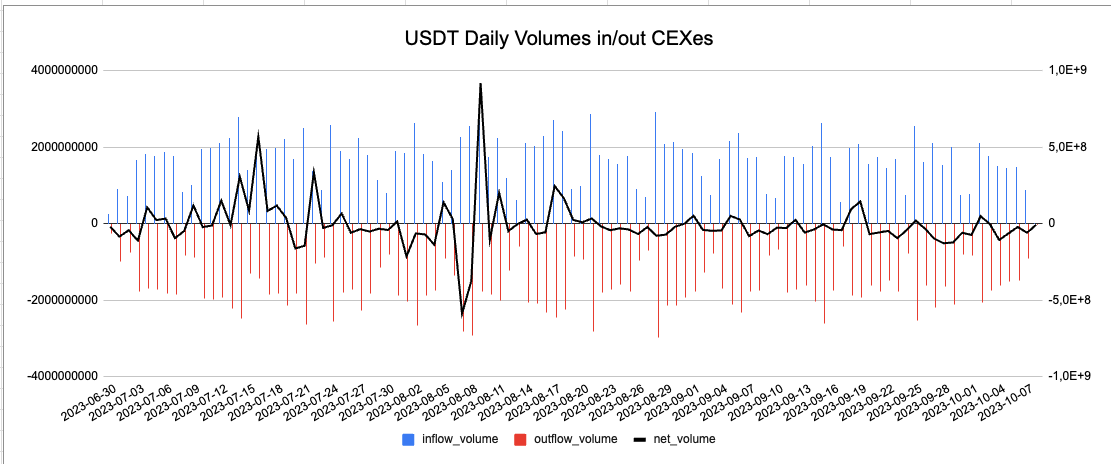

USDT Daily Volumes in/out CEXes:

- Inflow Volume (Blue Bars):

- Represents the volume of USDT being sent to centralized exchanges (CEXes).

- There are periodic peaks, indicating days with higher inflow than average.

- Outflow Volume (Red Bars):

- Denotes the volume of USDT leaving centralized exchanges.

- Similar to inflow, there are periodic spikes in outflow volume.

- Net Volume (Black Line):

- Shows the difference between inflow and outflow.

- It hovers around the zero mark but occasionally dips or rises sharply, indicating significant net outflows or inflows on those days. For instance, around the date 2023-08-14, there's a sharp negative dip indicating more USDT left the CEXes than entered.

USDT Daily Transaction number to/from CEXes:

- Inflow Transactions (Blue Bars):

- Represents the number of transactions sending USDT to CEXes.

- There's a consistent trend of inflow transactions with some minor daily variations.

- Outflow Transactions (Red Bars):

- Number of transactions sending USDT out of CEXes.

- Like inflow transactions, the outflow transactions follow a consistent trend with minor daily fluctuations.

Key Observation:

- The inflow and outflow volumes seem to counterbalance each other most of the time, keeping the net volume relatively stable. This suggests an active and liquid market where USDT is frequently moved in and out of exchanges.

- The number of outflow transactions is usually twice bigger than the number of the inflow transactions, indicating that each deposit is either converted to assets or Fiat on exchanges, or used to split into at least 2 smaller portions. At the same time, assuming the volumes are counterbalanced, then the latter statement is valid.

- The weekly pattern observed on the Daily Volumes chart, where there's a noticeably larger volume during weekdays compared to weekends, suggests several factors at play:

- Operational Activities: Institutional players, OTC desks, or other large-scale operations might have more activities and transactions during the weekdays, as these are regular business hours for most regions.

- Trader Behavior: Individual traders might be more active during the week, with weekends reserved for rest or other non-trading related activities.

6.Travel Rule and Stablecoins Transfers

6.1. Scope Definition

For this particular research, we’ll try to analyse the possibilities to apply Travel Rule to the transactions with Stablecoins. Unlike in Fiat payment systems, blockchain doesn’t have a “payment details” field nor any information about transacting actors. This makes implementation of Travel Rule problematic if not impossible. But, most Users rely on 3rd party wallet/account providers to keep and operate their funds with, and these providers (especially CEXes) do KYC verification. The question is, can this information be queried somehow from these providers and will it be enough for implementing the Travel Rule?

6.2. Technical Details

First of all, we’ll assume that each Holder has a non-custodial wallet and an account on CEX. On both wallets (accounts) User keeps some amount of money. Account on CEX is verified, meaning that User has provided his KYC data and it’s been verified. With a non-custodial wallet, User keeps his privacy. No documents provided or data available to the provider of this wallet.

When User A wants to send Stablecoin to User B, he might choose to:

- Send directly from CEX account to CEX account of a counterparty

- Send from his non-custodial account to CEX account of counterparty

- Send from his CEX account to non-custodial account of counterparty (which is normally prohibited by Terms and conditions of CEXes, that states that users are allowed to deposit and withdraw to their personal addresses only)

- Make a direct transfer from non-custodial wallet to counterparty non-custodial wallet.

In terms of Travel Rule application:

- In this case we have information about both User A and User B

- In this case we have information about User B only

- In this case we have information about User A only

- No information about any users available

But in case we combine case 2 and case 3 (meaning, that User A withdrew from CEX to his/her non-custodial wallet, then sent money to User B’s CEX Deposit Address), Travel Rule implementation seems possible as well.

For purposes of this research, we’ll concentrate on case 1 and combined 2+3 case, then give an estimation of transaction number and volumes that are potentially suitable for Travel Rule implementation.

Token transactions and flows for both as well as some technical details and challenges are discussed in the following chapters.

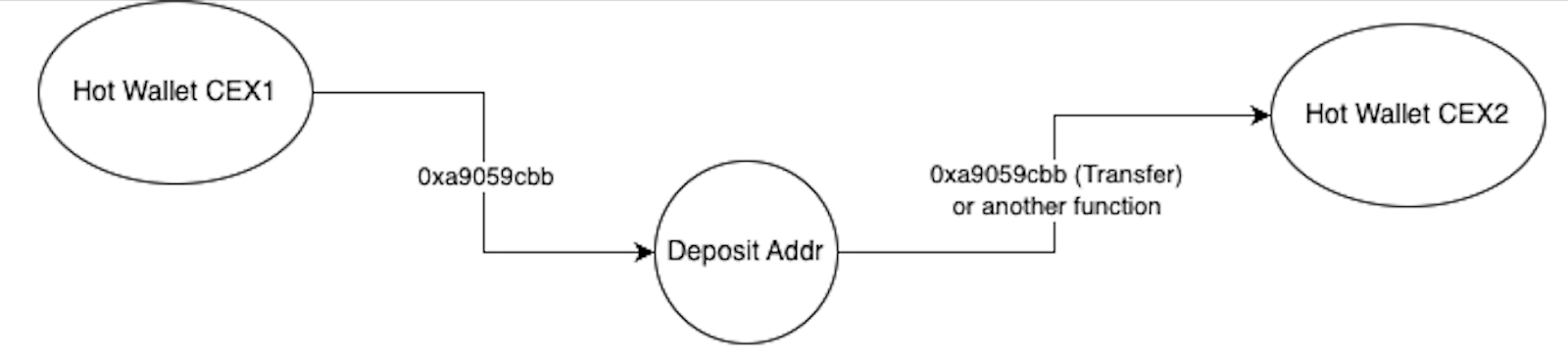

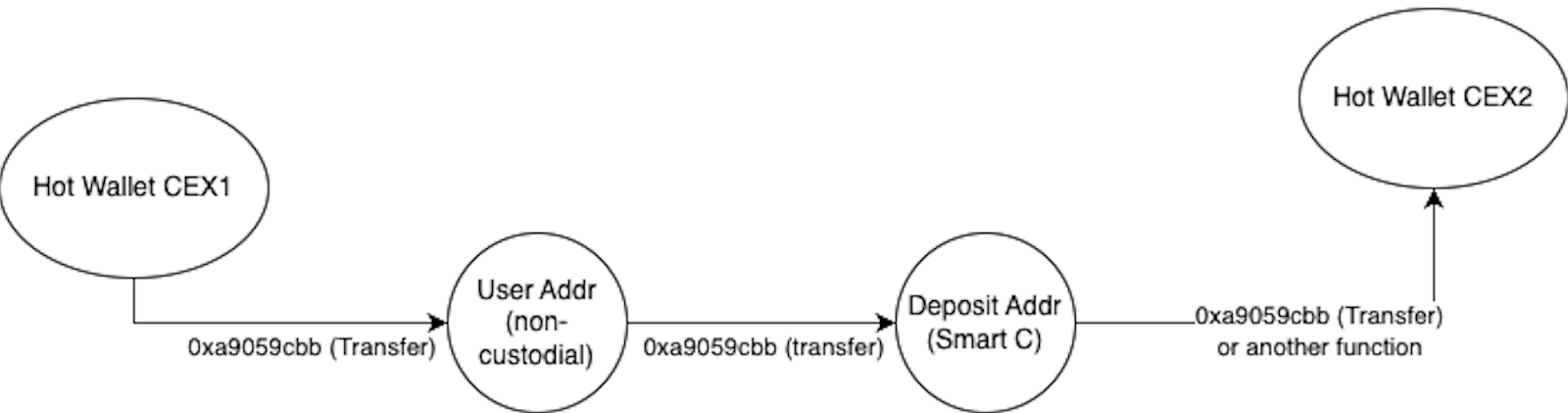

6.2. 1. Case 1. CEX => DepositAddr => CEX

When user A issues withdrawal from CEX account, it’s actually performed from a consolidation wallet (i.e. CEX 1 hot wallet). What user A normally does, is that he provides a so-called “withdrawal address”. This way the CEX 1 information system understands where to send funds. In Case 1 user A provides “Deposit Address” of user B on another CEX 2.

The behavior of the “Deposit Address” is under full control of the CEX information system. It is designed the way that it collects deposited funds to a consolidated account (Hot Wallet) ASAP. Practically, within minutes, but sometimes it may require 2-3 hours. Also, it will move exactly the same amount that User A deposited and then credit it to User B account, which is also very important to understand.

Sometimes User A sends a small amount of tokens to User B’s Deposit Address and waits for User B to confirm receival onto his CEX account. Then issues transfer of outstanding amount. Depending on CEX information system implementation, this results in 2 transactions issuing from CEX 1 Hot Wallet to Deposit Address, and only 1 “collecting” transaction from Deposit Address to CEX 2 Hot Wallet. In this case, it makes sense to count “transfers” based on “collection” transactions rather than “originating” transactions.

By understanding behavior patterns above, we can make 2 important conclusions that will simplify our research:

- It makes sense to analyze the last leg (a “collecting” transaction) in terms of transfer amount and date. First leg to be ignored, especially due to the fact that it may result in “duplicates”.

- Time difference of the 2 legs can be ignored. “Collecting ASAP” is practically done within minutes after deposit received, and definitely within the same business day.

6.2.2. Case 2. CEX => W => DepositAddr => CEX

This case is more complex compared to the previous one in terms of analysis. This case includes an intermediate wallet (W) that belongs to User A. Within this case the actual flow is the following:

- User B provides User A with his “Deposit Address” and requests a certain amount of funds (AMT) to be transferred.

- User A opens his/her account on CEX, but instead of doing direct transfer to Deposit Address, s/he decides to withdraw on his own intermediate address W.

- After withdrawal received to wallet W, User A initiates transfer of requested AMT to Deposit Address of User B

- When the CEX2 information system detects funds on Deposit Address, it triggers “collecting” transfer to CEX 2 Hot Wallet.

This case consists of 3 transactions, and the problem is that they might be separated in time and not equal in terms of transfer amount. It is very hard to “match” such transactions due to this fact. For the purposes of this research (which is estimation of the transaction amount that a Travel rule can be applied to), we consider making simplification assumptions that will not reduce the amount of transaction detected but may result in “false positives” detections which is a tradeoff we can make. The list of assumptions taken:

- We’ll base the calculations on the “collecting” transaction, same as we did for Case 1. We consider it’s reasonable because:

- Its amount is defined by User B who’s requesting payment. This is the only amount that makes business sense, no matter how much have User 1 originally withdrawn

- Business transaction (User A->User B transfer) is considered completed after “collecting” transactions are included and confirmed in the blockchain. Then CEX 2 can credit User B account.

- We’ll match transaction legs based on “addresses” only. No time or amount correlation applied. We consider it’s reasonable because:

- When User A withdraws to intermediate Wallet W, it’s usually User A’s wallet.

- If it’s not a User A address (User C, for example), User A knows exactly who this person is. Sending funds to random people is not practical.

- Even if User A is a OTC crypto trader which initiates CEX => W transfers for a large number of his customers, he knows their names too. Important point is will these customers transact with someone on CEX in future (perform W=> Deposit Address).

- User A may have some funds on W, so he might withdraw less funds from CEX1 then User B requested. Or even more funds (so that it will be enough for more transfers in future).

- This results in the fact that CEX1 => W transfer amount may differ a lot from originally requested User A->User B transfer

- CEX1 => W transfer may be significantly separated in time from actual User A->User B transfer we are interested in.

- Number of CEX1 => W transfers will never match the number of performed business transactions we are interested in.

- Amount transferred on Leg 2 (W=>Deposit Address) matches amount transferred on Leg 3 (Deposit Address => CEX 2 Hot Wallet) for the reasons discussed in Case 1. So time and amount of Leg 2 are not important for business transaction analysis.

By understanding behavior patterns above and taking into account assumptions, we can make 2 important conclusions that will simplify our research:

- It makes sense to analyze the last leg (a “collecting” transaction) in terms of transfer amount and date. First 2 legs are ignored, due to the fact that it may result in “duplicates”.

- Time difference of the legs can be ignored.

- Matching to be done based on addresses only.

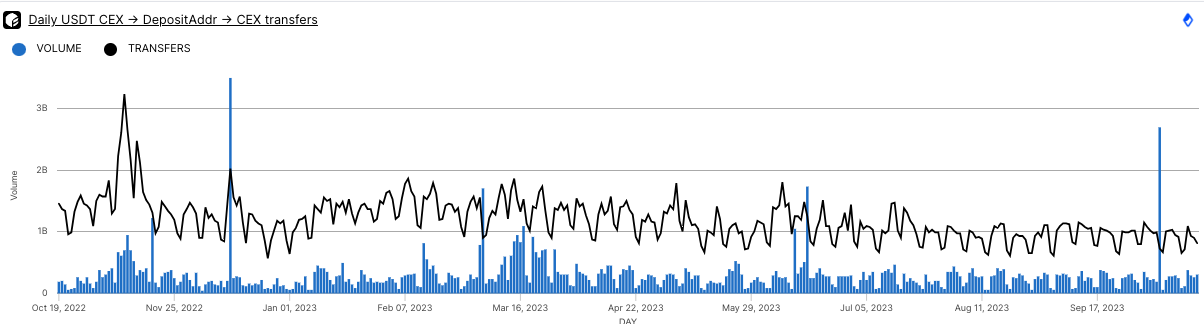

6.3. USDT Travel-Rule capable transactions in Ethereum

Case 1 (CEX -> DepositAddr -> CEX transfers):

- Volume (Blue Bars): The volume peaks are around 2.5B-3B and troughs seem to be around 1B. Averaging these, the estimated average daily volume is slightly above 0.5B USDT.

- Transactions (Black Line): The transaction count peaks are slightly above 10k. Averaging these gives an estimated average daily transaction count of around 4-5k.

- This case represents approximately 10-15% of total daily USDT transactions in Ethereum

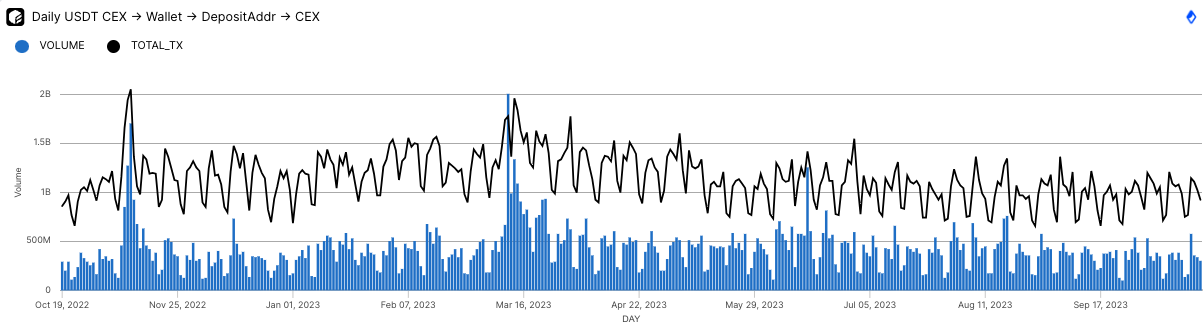

Case 2 (CEX -> Wallet -> DepositAddr -> CEX):

- Volume (Blue Bars): The volume peaks around 1.5B-2B and troughs are typically above 200M. Averaging the peaks and troughs gives an estimated average daily volume slightly above 1B USDT.

- Transactions (Black Line): The transaction line oscillates with clear weekly patterns, peaking around perhaps 15k and dipping to around 8k at the lowest points. Averaging these gives an estimated average daily transaction count of around 10k.

- This case represents approximately 7-10% of total daily USDT transactions in Ethereum

Comparison:

- Volume: The average daily volume for the CEX -> DepositAddr -> CEX pathway is higher, approximately by 200M USDT, compared to the CEX -> Wallet -> DepositAddr -> CEX pathway.

- Transactions: The CEX -> Wallet -> DepositAddr -> CEX pathway also witnesses a twice higher transaction count daily, compared to the CEX -> DepositAddr -> CEX pathway.

Both charts clearly display a weekly pattern, with higher activity during weekdays and lower activity during weekends, consistent with typical crypto trading behavior. The direct CEX -> DepositAddr -> CEX transactions have typically higher volume but twice smaller transaction counts compared to the transactions that involve an intermediate wallet.

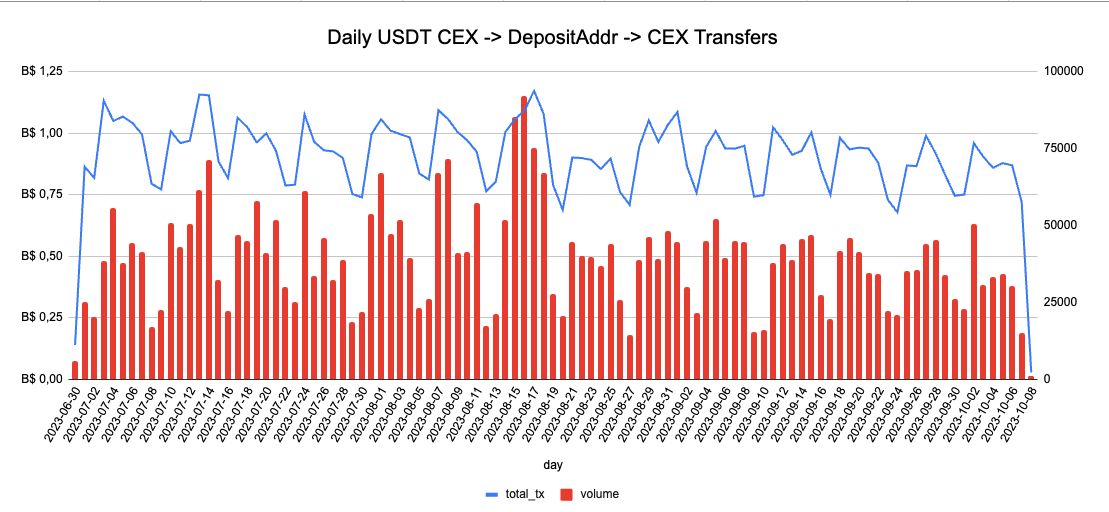

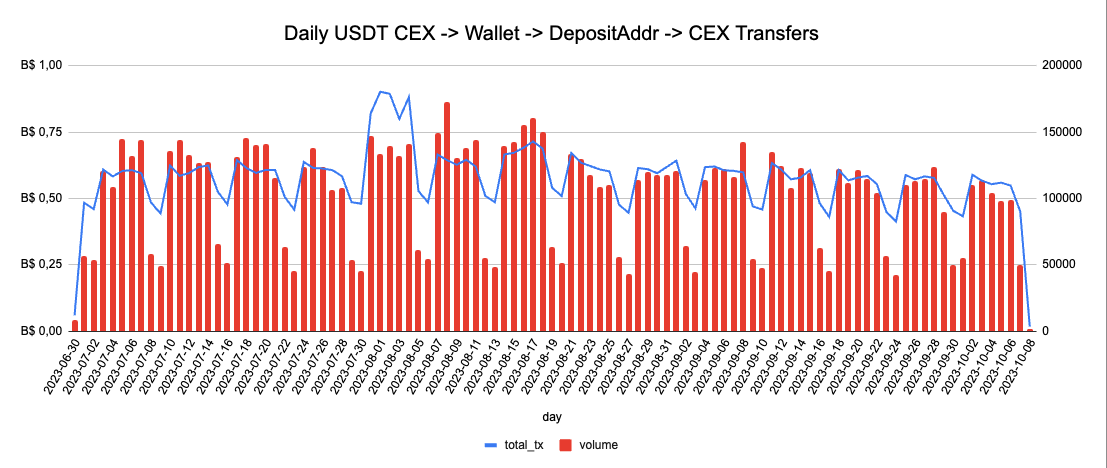

6.4. USDT Travel-Rule capable transactions in Tron

Case 1: CEX->DepositAddr->CEX

- Volume (Red Bars):

- Mostly fluctuates between 0.25 Billions USDT and BS 1.25.

- Average appears to be around 0.75 Billions USDT.

- Number of Transactions (Blue Line):

- Ranges roughly between 50,000 and 75,000.

- Average looks to be around 62,500 transactions per day.

- This case represents approximately 4-8% of total daily USDT transactions in TRON

Case 2: CEX->Wallet->DepositAddr->CEX

- Volume (Red Bars):

- Fluctuates roughly between 0.25 Billions USDT and 1.00 Billion USDT, with occasional spikes close to 1.00 Billion USDT.

- Average appears to be slightly below 0.50 Billions USDT.

- Number of Transactions (Blue Line):

- Oscillates approximately between 50,000 and 200,000, averaging somewhere around the middle.

- Average seems close to 125,000 transactions per day.

- This case represents approximately 4-5% of total daily USDT transactions in TRON

Comparison:

- Volume: The second chart (CEX->DepositAddr->CEX) tends to have a higher average daily volume at around 0.75 Billions USDT compared to the first chart's average of slightly below 0.50 Billions USDT.

- Transactions: The first chart (CEX->Wallet->DepositAddr->CEX) has a higher number of transactions per day, averaging around 125,000, while the second chart averages at about 62,500.

Both charts indeed have a weekly pattern, likely due to market activity being lower on weekends and higher on weekdays.

7.Conclusions

- Unlike Tron, Ethereum has significantly bigger DEX usage. Tron keeps its place on the OTC market instead.

- In both Ethereum and Tron USDC shows a recurrent weekly pattern of activities, especially on Direct Transfers. Such “background” activities don’t correlate much with trading events and market conditions, thus are inspired not by speculations on CEXes/DEXes, but by another type of user case (and therefore - businesses)

- Assuming CEXes are all regulated, with proper KYC and compliance procedures in place, Travel Rule can be enforced for no more than 20% and 12% transactions for USDT in Ethereum and Tron correspondingly.

- This is a top estimate due to assumptions taken in this research, practical results will give lower numbers,

- This requires a “communication layer” built between CEXes, which might be in different jurisdictions.

- The rise of Privacy Preserving protocols will reduce efficiency of open ledger based surveillance. Such protocols tend to integrate KYC providers nowadays, and perform KYC for their users. But they are not capable of providing any information that binds Input and Output from their pools and thus, can not enforce Travel rule technically.