AML Audit Checklist: How to Follow All the Regulatory Rules

Nowadays, anti money laundering programs are necessary to follow for every enterprise that deals with finances. There are a number of guidelines that regulate the area for AML activities. Failure to comply with these security policies and principles will lead your business to undermined trust and harmful sanctions from regulators.

As we know, ignorance of the law excuses no one. Still, how do you know that your company meets all the regulatory requirements? Just do some research and check your AML compliance. We did the first part, now is your turn to ensure your organization complies.

Key Takeaways

- AML compliance is essential for financial institutions to prevent money laundering, fraud, and terrorist financing.

- Non-compliance risks include significant financial penalties, reputational damage, and regulatory scrutiny.

- Key components include risk assessments, customer due diligence (CDD), transaction monitoring, and regular audits.

- AML compliance officers and staff training provides the effective implementation of policies.

- Advanced technologies like AI and robotic process automation (RPA) streamline compliance and enhance risk detection.

What is AML Compliance?

To prove that your business is one of the secure financial enterprises, there is a set of standards called AML compliance. Anti money laundering compliance policy is everything that the firms do to reduce scamming and personal data leaks. It includes the functions of:

- monitoring,

- reporting,

- regulations,

- and user-processing policies.

For comprehensive risk detection, the company must develop a program that explains the functions of immediate reports, risk management, and interactions with a person delegated for that.

Why do you need an AML compliance program?

First, it is a minimum threshold that guards your customers and prevents frauds. Secondly, it helps you to avoid possible sanctions from regulatory institutions. The lack of effective AML compliance programs has led regulators to impose fines of millions against companies, depriving them of considerable financial resources.

While the AML sanctions in 2018 were around four billion dollars, the penalties for non-compliance increased to the value of almost $8 billion in 2019. Such figures come from the shared ignorance on the questions of financial fraud and jurisdiction. The Payments Cards & Mobile report evidences that the USA has the biggest percentage of financial frauds around the world now. The United Kingdom takes second place. The record number continues to grow each year.

Such a tendency gives a number of scopes for creating new AML solutions. According to other resources, the global market is expected to grow from one billion dollars in 2019 to five billion in 2027. Moreover, the epicenter of the AML market will remain in the region of North America and the Pacific.

Currently, this problem is not common only for banks. The biggest share of the penalties has been given to them in retrospect. In 2019, this share was less than 50%. It evidences that the money laundering problem has become a shared issue for all businesses. The previous year has also received a record number of AML compliance penalties.

Assessment of risks for the program

It is the most significant part of our checklist. For risk assessment, you need to cluster customers into risky and not-risky ones. A number of tools can help you to organize all the data. For instance, the ML\TF risk assessment methodology detects potentially dangerous affairs. Consider the main possible risk factors like:

- countries of transactions,

- resources of income

- PEPs (politically exposed people). It stands for significant social figures within a state or in the global arena.

- and UBOs (Ultimate Beneficial Owners), also known as the final beneficiaries. That is the parties that benefit from the banking manipulations and may hide their resources of profit by a number of operations, just literally “laundering” them. In this way, it is extremely hard to find the roots of funds. The regulatory requirements for fintech firms struggle to not allow the clients to create those layers.

Don’t forget about Know Your Customer KYC policies for knowing the financial background of your clients. Besides, do not forget to ensure that your clients have their rights reserved. Most importantly — your compliance program should function along with your business’ needs.

AML compliance audit

Test your future program! You should clearly understand that you cannot ensure your AML compliance policies without practicing auditing. It is the overall assessment of a company’s activity, security measures, reporting, and accounts. The organization named Crowe Horwath Bank reports that the Federal Financial Institutions Examination Council (FFIEC) suggests financial institutions to make independent testing every year, or even more frequently. To be objective, you should involve the services of third party organizations that have a big experience in auditing and risk management.

AML compliance officer

If you run a business, it shouldn’t be solely your responsibility for the security of the services you offer. Instead, hire an employee who will be in charge of the process! A compliance officer is somebody on your team who has the expertise and experience to lead the risk management team and make recommendations on effective audits. Most often, the specialist leads the AML compliance processes when it comes to the professional training of employees about security in general and AML procedures specifically.

A number of corporations whose activity is not limited to financial functions (you have heard the names like Google, Apple, and Facebook) have long enjoyed the benefits of hiring a compliance officer. Such an expert also checks compliance with partnership conditions and follows all the changes in policies, both internal in a team and external with partners. Undoubtedly, this employee should have enough experience and ideally be a certified specialist.

AML compliance training

Another crucial point is reporting and onboarding control. The internal staff must ensure their roles and responsibilities in risk detecting and reporting financial crimes on time. That’s a good topic for discussion for your next training! Be sure to involve all the necessary ethical policies and compliance with them by employees.

Keep your team updated! It is advised to provide internal training on the AML compliance checklist among all staff members. Your employees should not only get the theoretical understanding but practice in their day-to-day working duties. Ideally, everybody in your company should meet onboarding training on preventing crime and money laundering.

What Are AML Documents Needed for Your Activity?

Nowadays, anti money laundering AML practices are obligatory for every financial organization. Adhering to them is not an option — you cannot run your business without the one. Since the global community has taken a risk based approach in preventing frauds and terrorism, each financial institution should ensure its potential in fighting money laundering.

It is why it is better to keep your team updated on the latest manuals and regulations on AML. For those states that belong to the European Union, there is the 5th AML directive that includes anti money laundering AML practices for the enterprises. As for the United States, the firms should adhere to several regulatory guidelines. The main ones include the Bank Secrecy Act and USA Patriot Act against terrorism, which was introduced after the 9\11 attacks in the States. Be also sure to get familiar with Money Laundering and Financial Crimes Strategy Act, Money Laundering Suppression Act and Intelligence Reform, and the latest Terrorism Prevention Act. Have a careful look at the other ones!

Depending on your specific activity and country, there is a common set of manuals and tools. You should carefully have your AML steps documented. At least, you must get a written AML compliance order. Check if your document provides the data on:

- AML regulatory policies, your organization complies with.

- Responsible team or person who will create the report in case of scam suspicion.

- Resources and tools for working with customers.

- Terms of fraud reporting.

- What do you define as suspicious activities and risks?

- How you will detect suspicious activity.

- Auditing and monitoring policy.

The aim of this step is to make effective standards for the whole organization. If you do not know where to start your way from, here you can review an AML compliance program template for small organizations. The AML compliance checklist should also fall under the requests of a particular jurisdiction.

If you are sure that your firm follows all the requirements, you can take the anti money laundering and Know Your Customer exam. It scores the level of competence on the questions of security and AML official guidelines among employees of banks and other similar institutions.

How to Prepare for the Exam?

Apart from the certification, the examining institutions often provide corresponding courses. The requirements for passing an exam may be different. The exam has two parts, including KYC and AML knowledge. As a rule, it covers the information about AML regulatory function and tools, international committees, and legal order of a particular country (or unit). You can also pass a number of mock exams first. They are specially created so that students can learn their level of knowledge before obtaining a certificate. Here is a sample of the AML KYC exam.

What Is an AML Checklist?

An anti-money laundering (AML) checklist is a framework designed to help financial institutions comply with regulatory compliance requirements to avoid money laundering, financial fraud, and terrorist financing within their business.

It includes processes like screening and verifying the identity of customers, assessing their risk level, monitoring transactions, and reporting suspicious activity.

The AML checklist assists companies in complying with laws such as the Bank Secrecy Act, FATF guidelines, and EU regulations (including MiCA). It preserves the stability and integrity of the financial system. Through the evaluation of customers' financial activities and transactional behavior, an AML checklist allows institutions to identify potential risks and respond to red flags preventing illegal activities from infiltrating operations.

Taking into account the growing sophistication of financial crime and the increasing fines for non-compliance — totaling more than USD 7 billion in 2023 — the AML checklists became essential tools that protect institutions from reputational, financial, and operational risks.

AML Compliance Checklist: Best Practices

AML regulations are constantly changing. To work more productively in the changing conditions, financial institutions should implement best practices to strengthen their AML compliance regulations.

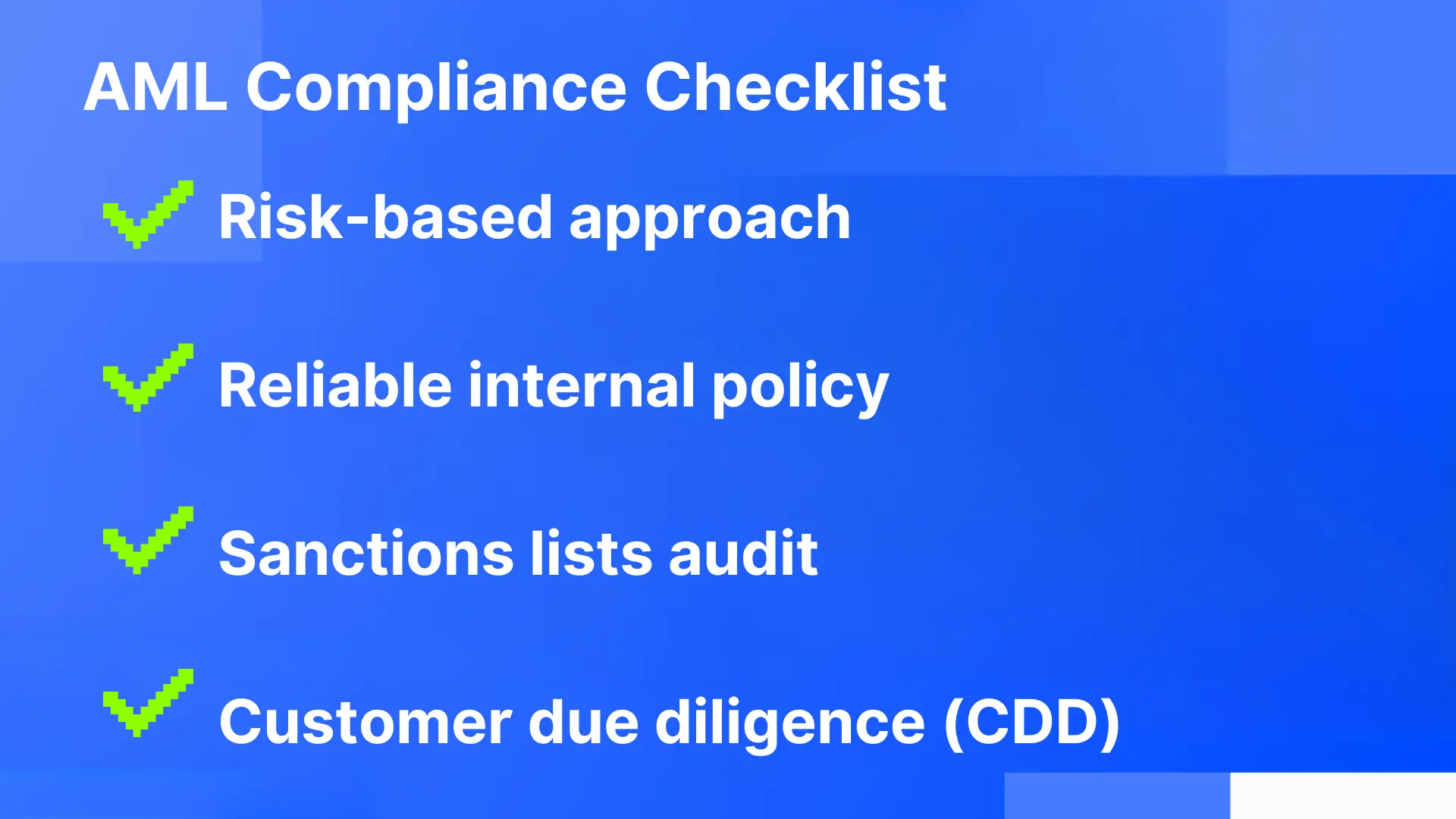

So, the AML checklist includes:

- Conducting a risk-based approach

Assessing the risks associated with the company's customers, the nature of their business, and profession. This also includes the assessment of cross-border transactions. Particular attention is paid to transactions in high-risk jurisdictions. For example, North Korea (sanctions), Iran (terrorism), Myanmar (deficiencies), Afghanistan (corruption), Russia (sanctions).

- Establishing a reliable internal policy

Develop clear internal guidelines for onboarding, transaction monitoring, and suspicious activity reports, ensuring that all internal controls are documented and regularly updated. Setting up such processes ensures that all employees can recognize red flags and report them on time.

- Check for compliance with sanctions lists

Regularly updating customer data. It is especially important to constantly check them for presence on international sanctions lists. The same applies to politically exposed persons (PEPs) and their partners.

- Customer due diligence (CDD) program

Verifying customer identity, assessing risk profiles, and performing enhanced customer due diligence (EDD) for high-risk customers and legal entities.

- Continuous monitoring of transactions

Automated systems are in place to identify unusual transactions that exceed regulatory norms and, accordingly, transactions from unfavorable jurisdictions.

In addition, the checklist should include employee training, proper documentation, and the use of AI and machine learning tools.

How would you detect the potential risks?

There are a number of “red flags” that identify that something may go the wrong way. Be especially careful regarding suspicious activity. To learn how to deal with similar cases, you should first understand how money laundering works. It involves activities that help to avoid law enforcement but still can be detected by AML compliance on time. Check it out:

- A large number of transactions

- Frequency of operations from one address to another

- Accounts associated with business, that have suspicious experience in laundering

- Large cash deposits or persistently large balances

- Ongoing address changes conducted to hide the funds’ resources

- Monetary activity, accumulated over a period of time (for example, individual transactions for a specific amount)

- Suspicious figures of UBOs, PEPs, and their onboarding accounts

It is just a short list of risky attributes. Besides, do not forget to learn the geography of transactions. Foreign transfers can also identify the potential risks on your platform. Some accounts can also become “dangerous” only in time. This is the evidence of why regular transaction monitoring is especially useful. To monitor means to make an ongoing review of your business’ activities. It will help find the probable changes in accounts’ activity.

Finding the atypical behavior can be a herald for criminal intentions. It is why you need to conduct constant monitoring as one of the AML tools. There are a number of activities to keep track of, including suspicious activities, change of policy, onboarding, market trends, new policies, and different transaction monitoring needs. Comprehensive monitoring helps you not only to ensure safety but keep abreast of new market trends and competitiveness.

Some institutions may also be involved in crime and money laundering. It is much easier for criminals if the directory or beneficial ownership involves people who perform criminal functions. Beneficial ownership also allows the frauders to overgo potential law enforcement in case of detection.

Therefore, it is essential to immediately report about suspicious activities to local Financial Intelligence Units. There are also a number of requirements for reporting. The most common are:

- Information about personality (identification) of the parties should be clearly established

- These parties should not know about suspicion

- There should be a delegated employee in charge for AML. The reports on suspicion should be written by a senior manager or other responsible person.

- You should include comprehensive information about why the transaction or the account should be considered as risky

- Appropriate data and the report should be directed to the corresponding regulators on time

One of the AML operations includes Know Your Customer KYC policies. They were authorized by the Bank Secrecy Act and the USA Patriot Act. It is the regulation that any financial institution must abide by. It means that you should identify your customer with specific requirements until you provide them with the banking tools, and consists of three stages: CIP, CDD, and EDD.

The Customer Identification Process (CIP) technology verifies a customer as a real person. For this aim, your program requests their name, ID number, place of living, date of birth, etc. per particular requirement. Here the detection of the first risk factors begins. Firms can do this by using independent and legal identification documents.

As long as you have identified the personality of your customer, it needs to proceed with Customer Due Diligence. It allows you to know if you can trust them — not just asking their name or date of birth. This is where you will need to implement your Know Your Customer check. Depending on the multiplicity of the customer’s check, you can apply Simplified Due Diligence, Basic Customer, or Enhanced one. The Simplified Due Diligence is a function used when the risk chances are low. It is not even required. The definition of SDD was coined in 2007 to describe the situation when the customer does not need the standard verification. In this case, the business is assured that the client falls under the needed categories and has all the needed information. On the contrary, the technology of Enhanced Due Diligence (EDD) requires creating the expected pattern of activity for customers of the highest risk. You may also need to implement Watch List Filtering tools using them to score customers from the most to least risky ones.

AML Compliance in 2025: Expecting Risk Growth

As we approach 2025, compliance with anti-money laundering legislation is becoming increasingly complex. Financial criminals are evolving along with monitoring tools.

That is why financial institutions are expected to face increased regulatory scrutiny. This will require the introduction of modern technologies such as artificial intelligence (AI) and machine learning (ML).

In fact, as early as 2023, 62% of financial institutions were using AI and ML to combat money laundering. This figure is expected to rise to 90% by 2025.

The proliferation of transactions through online banking and cloud computing creates new challenges. Therefore, companies will integrate real-time risk assessment tools and automated compliance mechanisms.

In 2024, overall illicit activity in crypto declined by nearly 20%, but stolen funds and ransomware surged. Stolen funds inflows doubled to $1.58 billion, and ransomware payments hit record highs, including a $75 million payment. Attackers increasingly targeted centralized exchanges, using advanced tactics like social engineering. Despite more frequent ransomware attacks, victims are paying ransoms less often, reflecting improved preparedness. Legitimate crypto usage reached its highest levels since 2021, driven by regulatory advancements and growing adoption.

The establishment of bodies such as the European Anti-Money Laundering Authority (AMLA) underscores the global commitment to strengthening anti-money laundering and enhancing regulation.

FAQ

What Is an AML Checklist?

An AML checklist is a structured framework that helps financial institutions comply with anti-money laundering regulations by verifying customer identities, monitoring transactions, assessing risks, and reporting suspicious transactions to prevent financial crimes.

How to Check AML Compliance?

AML compliance can be checked by conducting risk assessments, ensuring customer due diligence (CDD), monitoring transactions for suspicious activity, screening against sanction lists, and performing regular reviews of internal audits.

What are the Five Pillars of AML Compliance?

The five pillars of AML compliance are:

- Risk Assessment — identifying and mitigating potential risks.

- Customer Due Diligence (CDD) — verifying client identities.

- Transaction Monitoring — detecting unusual activities.

- Reporting Suspicious Activities (SAR) — filing reports to regulatory authorities.

- Training and Governance — educating employees and maintaining internal controls.