How to Choose an AML Platform for EU Crypto Compliance in 2026

On 17 April 2026, the European Securities and Markets Authority confirmed that the MiCA transitional period across the EU will officially expire on 1 July 2026 — after which any entity providing crypto-asset services without a CASP authorization will be in breach of EU law.

For the roughly 1,200+ virtual asset service providers that operated in the EU before MiCA, that deadline is not just a licensing event. It is the moment when supervisors, banking partners, and counterparties start expecting operational AML/CFT controls to be visible, documented, and reproducible on demand. In practical terms, knowing the MiCA Regulation Requirements for Crypto Businesses is no longer enough. The CASP also needs a working AML stack underneath the license.

This guide is written for that reality. It is not another walkthrough of MiCA. It is a buyer-side guide for compliance leads and operations teams choosing an AML platform that supports MiCA-era workflows — wallet screening, KYT, transaction monitoring, Travel Rule data, alerts, case management, audit trails, and the API integration that turns all of that into an actual production process rather than a slide deck.

Why EU Crypto Compliance in 2026 Requires an AML Platform, Not Just Legal Awareness

EU crypto compliance in 2026 sits on three overlapping legal pillars, and each one creates obligations that have to be operationalized, not just understood:

- MiCA (Regulation (EU) 2023/1114): The CASP authorization regime, governance requirements, operational controls, and ongoing supervision framework. Main CASP rules have applied since 30 December 2024; the transitional period for legacy providers ends 1 July 2026.

- EU Transfer of Funds Regulation (TFR, Regulation (EU) 2023/1113): The EU's operational version of the FATF Travel Rule for crypto-asset transfers. EBA Travel Rule guidelines applied from 30 December 2024 and shape how CASPs collect, transmit, and validate originator and beneficiary information.

- AMLR and AMLD6 (Regulation (EU) 2024/1624 and Directive (EU) 2024/1640): The unified EU AML/CFT rulebook and the directive on national supervision. They fully apply from 10 July 2027, but AMLA — operational since 1 July 2025 — is publishing technical standards through 2026 that will shape implementation.

2026 is the year compliance teams have to act, not wait. AMLA's own work programme requires roughly 23 Level 2 and Level 3 measures to be published before the AMLR application date, with most of them due by mid-2026.

That sequencing matters for tool selection. A CASP that picks an AML platform purely against today's rules will find itself re-tooling within a year. A platform chosen against the direction of MiCA + TFR + AMLR — with room for the AMLA technical standards still being drafted — is the more defensible bet. For background on each pillar, see our explainers on the MiCA License for CASPs, the EU Crypto Travel Rule for CASPs, and how AMLR Changes KYC Obligations for Crypto Businesses.

The recurring AMLA message into 2026 has been blunt: crypto-asset supervision is a priority risk area, and obliged entities are expected to have strong, demonstrable AML/CFT protections in place. "Demonstrable" is the operative word — it means evidence in a system, not assurances in a policy document.

What an AML Platform for EU Crypto Compliance Should Actually Cover

An AML platform for EU crypto compliance is a set of connected capabilities that together let a CASP turn legal obligations into a repeatable operational process. The capabilities below are the ones that show up consistently in supervisory expectations and in serious counterparty due diligence.

Wallet Screening and Risk Scoring

Wallet Screening is the entry point. It assesses the on-chain risk profile of an address or counterparty — exposure to sanctioned entities, darknet markets, mixers, hacks, fraud clusters, ransomware payments, scam-related services, and other categories of high-risk counterparties.

In practical terms, useful wallet screening for an EU CASP needs three properties: comprehensive coverage of major chains and asset types (including stablecoins, which the FATF March 2026 stablecoins report flagged as the dominant settlement medium for illicit on-chain activity), transparent risk scoring methodology (so a compliance officer can explain why an address scored high during a regulator review), and continuous updates (because attribution data changes daily as new clusters are identified). No screening tool is 100% accurate, and a single check at deposit time does not substitute for ongoing monitoring — but a strong wallet screening layer is the floor.

Transaction Monitoring and KYT

KYT (Know Your Transaction) extends screening from a single-point check to ongoing analysis of behavior. It looks at transaction patterns, counterparty risk over time, threshold breaches, structuring patterns, sudden changes in activity, exposure shifts, and connections to newly identified risk clusters.

In practical terms, continuous transaction monitoring is what gives a CASP early warning. A wallet that was clean at deposit may later receive funds from a sanctioned address; a customer with a low risk score at onboarding may begin moving funds in patterns that suggest layering; a counterparty exchange may be downgraded after a high-profile incident. Without ongoing KYT, all of that is invisible until a regulator, banking partner, or counterparty surfaces it — usually at the worst possible moment.

KYC/KYB and Travel Rule Data Connection

The Travel Rule changed the data model of crypto AML. Before the TFR, customer identity (KYC) and transaction data (KYT) typically lived in separate systems. After the TFR, originator and beneficiary information has to travel with the transfer — which means identity data and transaction data must be linked in a single workflow.

An AML platform that helps a CASP comply with EU Travel Rule expectations needs to connect customer identity (for individual customers), business verification (for KYB), counterparty data (the receiving VASP or self-hosted wallet attribution where required), and transaction context. The harder this connection is to make inside the platform, the more manual the workflow becomes — and manual Travel Rule workflows do not scale.

Case Management, Audit Trails, and Reporting

Alerts without case management are noise. Case management is the structured process by which a compliance team triages, investigates, documents, and resolves alerts — and the audit trail is what proves to a supervisor, an auditor, or a banking partner that the process actually happened.

In reality, supervisors and banks increasingly expect to see four things in any AML case: who reviewed the alert, what data they considered, why the decision was made, and what action was taken (escalation, SAR/STR, customer off-boarding, no action with rationale). A platform that records all four in a way that can be exported and reproduced under examination is doing real work. A platform that just generates alerts and leaves the rest to spreadsheets is creating a future audit problem.

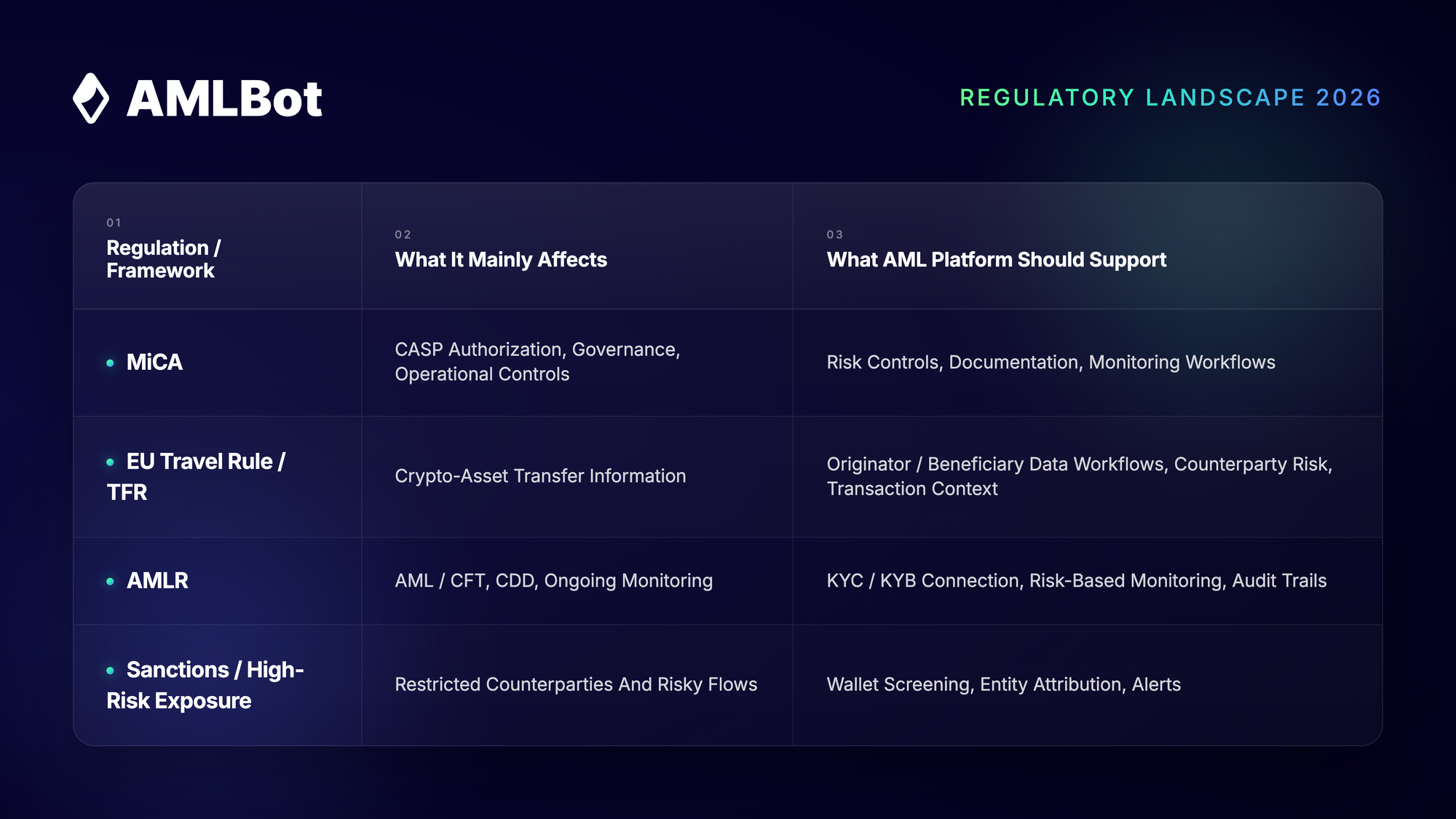

MiCA, EU Travel Rule, and AMLR: Which Tool Covers Which Requirement?

A common mistake is treating MiCA, TFR, and AMLR as a single undifferentiated "EU Crypto Regulation." They are different instruments, with different scopes, and an AML platform supports each one in different ways. Mapping the relationship is the easiest way to avoid both over-buying and under-buying.

The matrix above maps each regulatory pillar — MiCA, TFR, AMLR, and sanctions exposure — to the AML platform capability that operationalizes it.

The platform does not produce the legal status — it produces the evidence and the workflow. Legal status comes from the authorization, the policies, the staffing, and the supervisor's judgment. For Travel Rule, in particular, the operational complexity is its own subject; see EU Crypto Travel Rule Implementation Challenges for the practical issues teams run into when connecting counterparties across jurisdictions.

Best MiCA-Compliant AML Solutions for EU Crypto Businesses: What to Look For

There is no officially "MiCA-Compliant" AML software. MiCA does not certify tools and does not maintain an approved-vendor list. When industry sources and marketing materials talk about a "MiCA-Compliant AML solution," they mean a platform that supports the AML, KYT, monitoring, and evidence requirements that a MiCA-authorized CASP needs to satisfy in practice.

The right way to evaluate an AML platform for EU crypto compliance is against a set of operational selection criteria rather than a single label. The criteria that consistently matter:

- EU CASP Use Case Coverage: The platform should explicitly address the CASP business model (exchange, custody, transfer, advice, portfolio management) and the obligations attached to it under MiCA + TFR + AMLR.

- Wallet Screening Depth: Multi-chain coverage, stablecoin coverage, granular risk categories (sanctions, darknet, mixers, scams, fraud, ransomware, hacks, high-risk services), and transparent scoring.

- Continuous Transaction Monitoring: Not just deposit-time checks, but ongoing review of customer activity, counterparty drift, and exposure changes.

- Transparent Risk Scoring: A compliance officer should be able to open any alert and explain to a supervisor why the risk was assigned. Black-box scoring fails this test.

- API-First Integration: The platform should connect to onboarding, deposit, withdrawal, and internal compliance systems without manual data shuffling.

- Alert Workflow and Case Management: Triage, assignment, investigation, decision recording, and resolution all happen inside the platform.

- Travel Rule and KYC/KYB Compatibility: Identity data, business verification, and counterparty data should connect to transaction context inside one workflow.

- Audit Logs and Reporting Support: Every action should produce a record that can be exported for examination, internal audit, or banking partner review.

- Support for Compliance Teams, Not Only Engineers: The day-to-day users are MLROs and analysts. The interface, dashboards, and case workflow should be usable by them without ongoing engineering involvement.

- Ability to Scale From Manual Review to Automated Monitoring: A platform that fits a small team today should still fit when transaction volume grows by 10x.

For a broader view of how these criteria fit into AML programs beyond Europe, see our Crypto AML Compliance Guide for Businesses.

A note on labels: phrases like "MiCA-Certified," "Regulator-Approved," and "Guaranteed Compliance" do not describe a regulatory category that exists. Treat them as marketing language. The substantive question is always whether the platform produces evidence that satisfies the CASP's home regulator, AMLA's emerging technical standards, and the banking partners that the CASP depends on for fiat rails.

API Integration: Why It Matters for EU Crypto AML Compliance

For crypto exchanges, wallets, payment providers, and high-volume CASPs, manual AML checks become a bottleneck very quickly. A team that processes a few hundred onboarding decisions and a few thousand transactions per day can run on dashboards. A team that processes ten times that volume cannot. API integration is what turns AML controls into infrastructure. The typical workflow looks like this:

- Check Wallet Before Deposit: The deposit flow queries the AML platform synchronously, receives a risk score, and either accepts the deposit, holds it pending review, or rejects it.

- Screen Withdrawal Address: The withdrawal flow validates the destination address against sanctions and high-risk categories before the transaction signs.

- Monitor Transactions After Onboarding: Ongoing customer activity feeds into the platform, where rules and analytics flag patterns of interest.

- Trigger Alerts When Risk Scores Change: A customer or counterparty that becomes higher-risk over time triggers a review, even if no individual transaction breached a threshold.

- Connect AML Data With Internal Systems: Risk data flows into the CRM, the compliance case system, and the customer support tools that need it.

- Keep Logs for Audit and Review: Every API call, decision, and override is recorded in a way that can be reproduced under examination.

In practice, AML API Integration for crypto businesses is what makes the difference between a compliance team that scales with the business and a compliance team that becomes the business's permanent bottleneck. It is also what most banking partners and institutional counterparties expect to see by the time a CASP reaches meaningful volume.

How to Choose an AML Platform by Crypto Business Type

Not every CASP needs the same configuration. The right platform depends on the business model, transaction volume, customer base, and risk exposure. Four common archetypes:

Crypto Exchanges and Trading Platforms

Exchanges need the broadest functional coverage: transaction monitoring across deposits, trades, and withdrawals; wallet screening on every inbound and outbound address; user risk profiles that update over time; alert workflows that scale to high alert volumes; and audit history that ties every decision to a specific reviewer. Exchange compliance lives and dies by the alert-to-action ratio. A platform that generates 10,000 alerts a day and gives the team no way to triage them efficiently is worse than a tighter, more explainable model that produces 500 alerts a day with clear context.

Custodians and Wallet Providers

Custodial businesses focus more on source and destination of funds, wallet risk, counterparty exposure, and ongoing monitoring of held assets. Because custodians often handle larger individual balances, the consequences of a single missed exposure are higher than at a retail exchange. A separate point worth handling carefully: whether a non-custodial wallet provider is in scope depends on the specific services offered and on local interpretation. The honest framing is that classification varies, and that any wallet provider should get jurisdiction-specific legal input rather than assume coverage either way.

Crypto Payment and Transfer Providers

Payment and transfer providers feel the Travel Rule and sanctions exposure most acutely. Originator/beneficiary data has to flow with the transfer, merchant and customer risk needs to be assessed in near-real time, and the cross-border transaction context (counterparty VASP, jurisdiction, transfer size) drives most of the compliance decisions.

These providers benefit most from a platform where Travel Rule workflows are part of the AML stack, not a separate bolt-on system that has to be reconciled later.

Smaller CASPs and Startups

Smaller CASPs typically need simplicity of deployment, a clear dashboard, fast review workflow, API integration that does not require a dedicated engineering team to maintain, and compliance evidence that does not require enterprise complexity to produce.

The realistic framing is that manual review may work in the earliest stages, but risk and complexity grow with transaction volume — and the cost of switching platforms later is meaningful. Choosing a platform that fits today but can scale tomorrow is a better trade-off than buying for current volume and re-tooling within a year.

Common Mistakes When Choosing AML Tools for Europe

A handful of mistakes show up repeatedly in CASP procurement decisions. Each one creates either a compliance gap, a procurement regret, or both.

- Choosing KYC Without KYT: Identity verification at onboarding does not tell you what the customer does next. A program with strong KYC and no transaction monitoring fails ongoing-monitoring obligations.

- Relying Only on One-Time Wallet Checks: An address that is clean today can interact with a sanctioned counterparty tomorrow. Continuous monitoring is what catches the change.

- Ignoring Travel Rule Workflows: Treating TFR compliance as a separate project from the AML stack creates parallel systems that have to be reconciled manually — exactly where errors happen.

- Not Keeping Audit Trails: Decisions that cannot be reproduced under examination are decisions that cannot be defended.

- Using Risk Scores Without Understanding Them: A platform whose scoring methodology cannot be explained to a supervisor will not survive a difficult review.

- Choosing a Tool That Cannot Integrate via API: Manual data shuffling becomes a permanent operational tax that grows with volume.

- Treating MiCA, TFR, and AMLR as Separate Silos: They overlap in practice. A platform that handles one but ignores the others creates blind spots at the intersections.

- Buying Enterprise Analytics When the Team Needs Operational Workflows: Some platforms are built for investigations teams at law enforcement or large banks. CASPs typically need operational AML workflows, which is a different product even when the underlying data overlaps.

AML Platform Checklist for EU Crypto Businesses

A short, actionable checklist for procurement. Before choosing an AML platform, confirm it can:

- Screen Wallets and Counterparties: Across the chains and asset types the CASP actually handles.

- Monitor Transactions Continuously: Beyond deposit-time checks, with rules and analytics that flag pattern changes.

- Explain Risk Scores: Provide visibility into why a score was assigned, with supporting attribution data.

- Connect KYC/KYB Data With Transaction Risk: Identity, business verification, and on-chain risk linked in one workflow.

- Support Travel Rule Workflows: Originator/beneficiary data handling, counterparty checks, and self-hosted wallet attribution where required.

- Create Alerts and Cases: With triage, assignment, investigation, and resolution recorded inside the platform.

- Keep Audit Logs: Exportable, reviewer-attributable, and reproducible under examination.

- Integrate via API: With onboarding, deposit, withdrawal, and internal compliance systems.

- Support Compliance Review: Usable by MLROs and analysts without ongoing engineering work.

- Scale With Transaction Volume: From manual review to automated monitoring as the business grows.

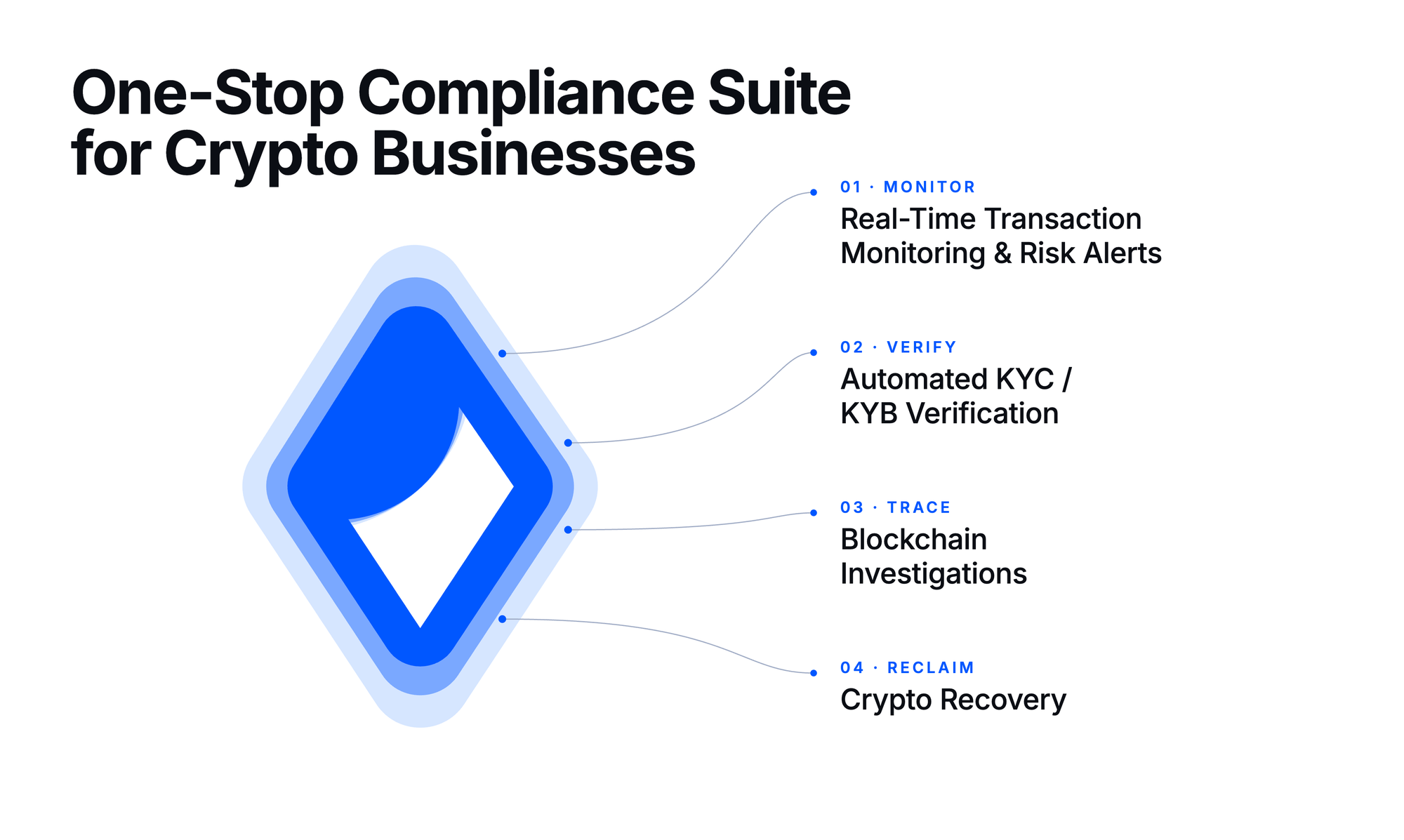

Where AMLBot Fits in EU Crypto AML Workflows

AMLBot supports EU crypto businesses with the operational layer that sits between the rulebook and the compliance team's day-to-day work: wallet screening, transaction monitoring, KYT workflows, risk scoring, API integration, and compliance review processes. The focus is on helping operational teams turn AML obligations into repeatable workflows — checks at the right point in the lifecycle, alerts with usable context, decisions recorded with their reasoning, and evidence that holds up in front of supervisors and banking partners.

The realistic framing matters: AMLBot does not deliver MiCA authorization, does not replace legal counsel, and cannot guarantee compliance by itself. What it does is support specific controls inside the CASP's Compliance Program — particularly Wallet Screening and Transaction Monitoring Tools that fit into existing onboarding, deposit, and withdrawal flows through APIs.

The four modules above cover the operational workflows small and mid-sized CASPs need most in practice: ongoing transaction monitoring, identity and business verification, on-chain investigations, and recovery support — in one stack rather than across four separate vendors.

In real-world terms, the question for a CASP is whether the platform fits the actual compliance workflow the team needs to run — not whether the platform carries a regulatory label that does not exist.

Conclusion: AML Platform as the Operational Layer of EU Crypto Compliance

Choosing an AML platform for EU crypto compliance is about choosing a system that connects regulation, customer risk, wallet risk, transaction monitoring, alerts, evidence, and automation into one workflow that the compliance team can actually run.

The three regulatory pillars set the requirements: MiCA defines the CASP framework, the EU Travel Rule shapes how data flows with transfers, and AMLR strengthens the AML/CFT baseline. The platform decision should be based on operational needs — coverage, scoring transparency, workflow usability, integration depth, and audit reproducibility — measured against the CASP's specific business model and growth trajectory.

For teams currently evaluating their AML stack, the practical starting point is a gap review: Do current tools cover wallet screening, KYT, Travel Rule data, API integration, and audit evidence at the level the business will need by mid-2026 and into the AMLR application date in 2027? The answers to that question are usually more useful than any vendor-led demo.

Follow/ Contact AMLBot:

🔗 Website

🔗 Support Team

🔗 LinkedIn

FAQ

What Is an AML Platform for EU Crypto Compliance?

An AML platform for EU crypto compliance is a tool or set of tools that helps crypto businesses screen wallets, monitor transactions, assess risk, manage alerts, keep audit records, and support compliance workflows under EU rules such as MiCA, the EU Travel Rule (TFR), and AMLR. It is the operational layer that turns regulatory obligations into repeatable processes evidence can be drawn from.

What Is the Best MiCA-Compliant AML Solution for EU Crypto Businesses?

There is no officially certified "MiCA-compliant AML solution" — MiCA does not approve specific software. The best AML solution for an EU crypto business depends on its model (exchange, custody, transfer, payments), transaction volume, risk exposure, jurisdictions of operation, and compliance team structure. Useful evaluation criteria include wallet screening depth, continuous transaction monitoring, transparent risk scoring, alert workflow, case management, audit trails, Travel Rule compatibility, and API integration.

Does MiCA Require Crypto Businesses to Use an AML Platform?

MiCA does not name a specific platform or mandate any particular AML vendor. It does require CASPs to maintain effective risk management, internal controls, monitoring, and documentation. For most CASPs, an AML platform is the practical way to operationalize those obligations and to produce the evidence that supervisors and banking partners expect.

What Is the Difference Between MiCA, the EU Travel Rule, and AMLR?

MiCA (Regulation (EU) 2023/1114) sets the EU framework for crypto-asset service providers, including authorization, governance, and operational requirements. The EU Travel Rule, under the Transfer of Funds Regulation (EU 2023/1113), governs the originator and beneficiary information that must accompany crypto-asset transfers. AMLR (Regulation (EU) 2024/1624) creates the unified EU AML/CFT rulebook, including customer due diligence, ongoing monitoring, and reporting obligations, and fully applies from 10 July 2027.

What Features Should an EU Crypto AML Platform Include?

An EU crypto AML platform should include wallet screening across relevant chains and assets, ongoing transaction monitoring with KYT capabilities, transparent risk scoring, sanctions and high-risk exposure screening, alert workflows and case management, audit trails, reporting support, KYC/KYB data connection, Travel Rule workflow support, and API integration with onboarding, deposit, withdrawal, and internal compliance systems.

Is Wallet Screening Enough for EU Crypto Compliance?

No. Wallet screening identifies risk at a specific moment but does not cover ongoing customer activity, counterparty drift over time, or pattern-based suspicious activity. EU crypto compliance also requires ongoing transaction monitoring, customer risk context, alert review, suspicious transaction reporting where applicable, and reproducible audit evidence.

Why Is KYT Important for EU Crypto Businesses?

KYT (Know Your Transaction) is important because EU AML obligations require ongoing monitoring of customer activity, not only identity verification at onboarding. KYT helps compliance teams detect suspicious patterns, track counterparty risk over time, flag exposure changes, and generate alerts that are tied to specific transactions and counterparties rather than only to customer profiles.

Why Does API Integration Matter When Choosing an AML Platform?

API integration matters because crypto businesses need AML checks embedded directly in operational flows — onboarding, deposits, withdrawals, transaction review, alert creation — rather than executed as separate manual steps. Without API integration, compliance becomes a manual workload that does not scale with transaction volume and creates reconciliation gaps between the AML system and the production environment.

How Should Smaller CASPs Choose an AML Platform?

Smaller CASPs should look for an AML platform that is practical to implement, usable by a small compliance team without dedicated engineering support, and capable of scaling without re-tooling. The minimum useful feature set is wallet screening, transaction monitoring, alerts, case management, audit trails, and API workflows — provided in a form that does not carry enterprise overhead the business does not yet need.

Can an AML Platform Guarantee MiCA Compliance?

No. An AML platform can support MiCA-era compliance workflows by providing the screening, monitoring, alerting, case management, and audit capabilities a CASP needs in practice. Compliance itself depends on authorization, internal policies, trained staff, documented risk assessments, governance, and supervisory judgment — none of which any platform can deliver on its own.